Personal Finances

Welcome to Thriving-Baby-Boomers – A Whole person approach to wellness

“Empowering others to take a balanced approach to their own health and wellness by focusing on all aspects of the whole person.’

“Focusing on the whole person to maximize health and wellness for life.”

TBB logo

Personal Finances for Baby-Boomers

According to Wikipedia, “Baby-Boomers are the demographic group born during the post–World War II baby boom, approximately between the years 1946 and 1964.”

However, according to The Strauss and Howe Generational Theory, Baby-Boomers are defined as people born between the years 1943 – 1960.

For my purposes, I will use the broadest range of Baby-Boomers, from 1943 – 1964. This means anyone ranging in age from 54 to 75 years old in 2018 is classed as a Baby-Boomer.

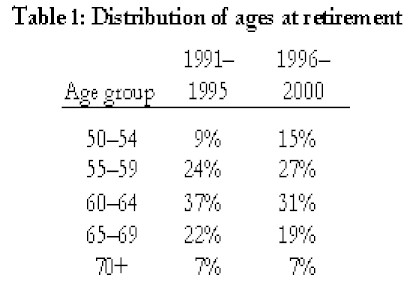

In the spring of 2003 Economica published a comparison over two 5-year periods (1991–95 to the five year period 1996–2000) to see if there was a rising or decreasing trend for the age of retirement in Canada. They found that up to 2,000 Canadians were retiring earlier than they did five years previous.

As shown in Table 1, in the five-year period 1991–95, the highest percentage of individuals retired in the 60 to 64 year age category. In the five-year period 1996–2000, 60 to 64 still remained the most popular age group for retirement; however, the percentage of individuals retiring within the age category had dropped by 6 percentage points (37 percent to 31 percent). The percentage of individuals retiring “earlier”, in the 50 to 54 age category and 55 to 59 age category both increased… This suggests that although many Canadians are still choosing to retire at “normal” retirement age (60 to 64), there is a shift to earlier ages.”

Table 1: Distribution of Ages at Retirement (years 1991 – 1995 and 1996 – 2000)

According to the chart above, eighty-three percent of retirees ranged in age from 55 to 69 during the period of 1991 – 1995. Whereas, during the period of 1996 – 2000, only seventy-seven percent of retirees fell into the same age range. The greatest increase of retirees was in the youngest category age range of 50 – 54 years old during the 1996 – 2000 time period.

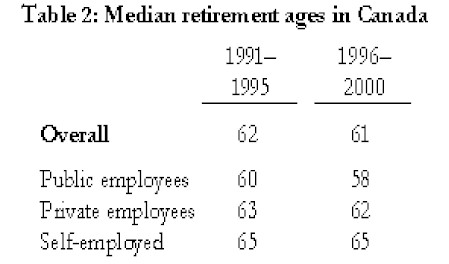

According to Economica, the average retirement age in Canada is somewhat dependent on whether one is employed in the public or private sector, or self-employed.

Table 2: Median retirement ages in Canada (years 1991 – 1995 and 1996 – 2000)

See the link for the complete analysis at Econimica.

According to a Canadian Business article, “Between 1976 and 2000, Canada’s average retirement age fell from 65 to an all-time low of 61.5, where it hovered for a decade.” They also stated, “In 1960 the average Canadian lived to age 71; today, a typical Canadian gets about a decade extra.”

The Canadian Business article produced quite a fascinating history of our OAS and CPP implementations throughout the years. It also discussed how better health care increases longevity and how the aging Baby-Boomers will affect the economy when so many are retiring.

Whether one had a well-paying job with good benefits, and managed to put money away in RRSPs or other forms of savings, or one will have to rely on OAS and/or CPP, Baby-Boomers have many opportunities to plan for their personal finances.

Many people of retirement age continue to work, whether full, or part-time. Others offer trades for their skills and services for useful products and services they desire.

Even if one doesn’t want the nine-to-five and commute, there are many ways Baby-Boomers can generate finances to and through their retirement. With so many talented and ‘crafty’ people and with Internet access, many Boomers can generate income by selling their products on sites such as e-Bay, Craigslist, Kijiji, Etsy, and many more.

My plan is to complete this website and create an online business offering products and services that I can sell whether I’m in front of the computer or not – this is called creating a passive income.

Here’s a great article with

16 Timeless Truths of Financial Freedom

STANDARD DISCLOSURE: In order to support my blogging activities, I may receive monetary compensation or other types of remuneration for my endorsement, recommendation, testimonial, and/or link to any products or services from this blog. Please note, that I only ever endorse products that are in alignment with my ideals and I believe would be of value to my readers.

Return to Financial Well-being

Return Home

Copyright © 2012 – 2022 thriving-baby-boomers.com. All rights reserved.

This website is for information purposes only and is not intended to be or to serve as, a substitute for legal, financial, or medical advice, diagnosis or treatment. Always seek professional advice.

Recent Comments